What You Need to Know About Millennial Women and the Wealth Gap

This is the first part of a year-long blog series that tackles the obstacles to wealth building that Millennial women face over their lifetimes. The goal is to unpack the forces that create the wealth gap for Millennial women and point to both practical advice and policy suggestions that can help create a more stable economic future for Millennial women.

Millennials get a bad rap. I know because I am one.

Granted, I was born in 1984, which puts me at the older end of the Millennial spectrum[1]–but, nonetheless, I’ve spent the last decade or so trying to establish my career and build a fulfilling personal life amidst both the economic realities and stereotypes of the Millennial generation.

We’re called “snowflakes” and criticized for wanting “safe spaces”, rather than celebrated for our activism and calls for diversity, inclusion, and accountability. We are told that our “frivolous” spending on things like soy lattes and avocado toast–which is delicious, by the way–is the reason for our dwindling bank accounts, rather than the realities of a workforce that is leaning more toward contract labor than retirement plans and pensions. Our selfie-strewn social media accounts are framed as signs of self-involvement and a disconnection from reality, rather than empowering, self-reflective, or community-building.

Our selfie-strewn social media accounts are framed as signs of self-involvement and a disconnection from reality, rather than empowering, self-reflective, or community-building.

But, the truth is that Millennials are much more complex and resilient than these cultural tropes make us out to be. There are nearly 75 million Millennials, making us both the largest and most diverse living generation to date. We are highly educated but are saddled with student debt due to drastic hikes in tuition costs. Yet, we earn the same, or sometimes less, than our parents did at our age. We came of age during a time of technological innovation and economic precarity (anyone remember the Great Recession?). A bleak analysis in a recent article proclaimed that “Eighties Babies Are Officially the Brokest Generation” and might never recover from the economic downturn that characterized our early working lives. These things add up, or, in the case of wealth…don’t.

While not an exhaustive list, many of these factors–an economic recession, the rising cost of living, educational debt, and increased economic inequality–have created a unique landscape for Millennials to navigate as we start our careers, build our families, and try to establish a secure economic future.

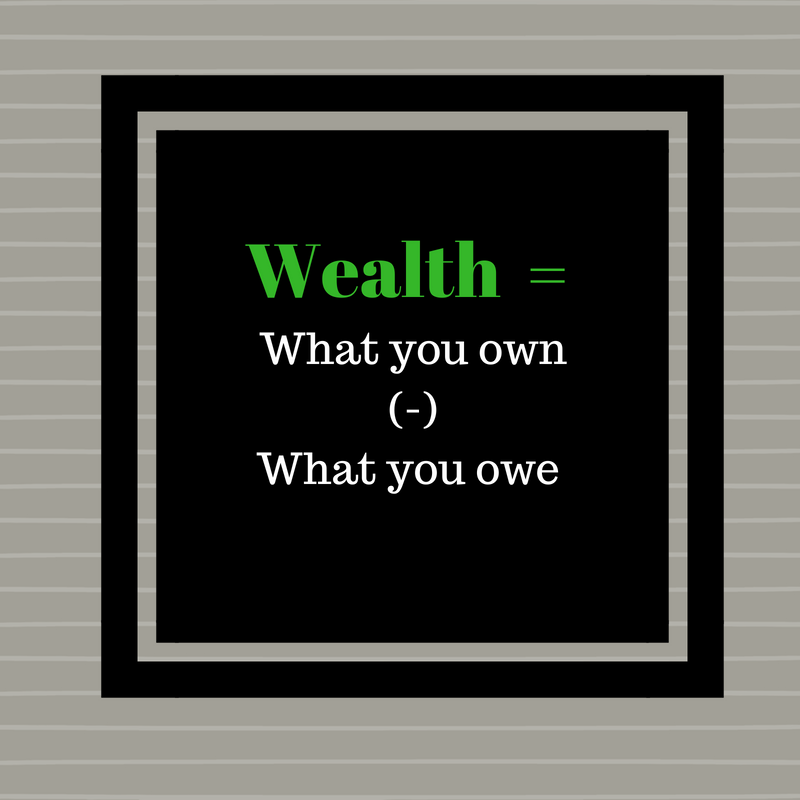

There are tangible ways to build economic opportunity, security, and access, starting with building wealth. But when we talk about wealth, what exactly do we mean? While the term might make you think of gold bars or stacks of one hundred dollar bills, wealth can be calculated using a simple equation: what you own minus what you owe.

Assets like homes, cars, businesses, property, retirement savings, and other investments work together to help people accrue wealth over time. Consumer and educational debt, mortgages, and fines and fees are liabilities that strip wealth.

The problem for Millennials is that we don’t often have the kind of assets needed to build wealth (there is some truth to that image of Millennials living in their parents’ basement, after all). And, because wealth begets wealth, we end up getting “stuck” or left behind, especially when compared to where our parents were at our age.

The widening wealth gap, not just between Millennials and their parents, but also between the richest and poorest Americans, is not a product of poor personal decision making but, rather, the effect of policy choices that have shaped who can build wealth in this country. A quick look back at our history reveals how policies like the G.I. Bill, which left out African Americans, and redlining, a Federal Housing Administration policy that classified neighborhoods according to their demographic makeup as a way to signal to banks where they should (and should not) invest, codified racist attitudes into law. On the other hand, legislation like the1974 Equal Credit Opportunity Act and No Fault Divorce laws, which sprung up in the late 1960s, pushed back against sexism and gave women a more defined pathway to financial independence.

Recent reports show that there is a staggering racial wealth gap, and it will take families of color generations to catch up to white families. The stark reality is this: In 2016, white families have an average wealth of $919,000, which is more than $700,000 higher than Black families ($140,000) and Latino families ($192,000).

The women’s wealth gap is also alarming. Women only own 32 cents for every dollar white, non-Hispanic men own. The accumulation of the gender pay gap, educational debt, low-wage and part-time work, caregiving responsibilities, and the rise in single motherhood make it hard for women to save for their retirement, not to mention other issues that might come up, ranging from a refrigerator repair to a major health emergency.

While the research focusing on the gender and racial wealth gaps is picking up steam, this blog series is meant to highlight the diverse lived experiences of Millennial women who have out-graduated men from college but still grapple with pay inequality as they enter the workforce; who are getting married later in life and find themselves in their prime childbearing years; and who comprise a growing percentage of the American workforce that is relying more heavily on “gigs” and contract labor.

Over the course of the next year, I’ll be unpacking some of the wealth-building barriers Millennial women face. Each blog will be dedicated to one factor of wealth—from intergenerational wealth, to homeownership, to retirement—offering both practical tips and policy solutions. This time next year you’ll—hopefully—be more in control of your own finances and have the tools to affect real change that helps close the wealth gap.

[1] Note: While there is some discrepancy about who counts as a Millennial, for the purposes of this blog I’ll be using the Pew Research Center definition, which counts Millennials as young people born between 1981 and 1996. For reference, the oldest Millennials will turn 37 this year.